Professor Kepler’s research studies how information shapes industrial organization both within and outside of firm boundaries

Information plays a critical role in the design on not only firms’ explicit but also implicit contracts in shaping firms’ disclosure and corporate governance practices. Professor Kepler’s recent work examines how companies use financial disclosures to strategically circumvent competition regulations and how disclosure regulations in the healthcare sector drive competitive behavior among firms.

His research on financial contracting and coordination provides evidence about the various mechanisms that work to facilitate contracting between firms. This includes M&A, strategic alliances, supply chain contracting, and other, less formal, interactions among competitors that firms can use disclosures to coordinate with.

His research on corporate governance practices focuses on how private information is used for contracting with managers—e.g., in bonus plans to align incentives of top management team members. His governance research also examines how and when the opportunistic use of information inside the firm might warrant regulation and enforcement.

His other related work provides practical briefs for both researchers and practitioners, with an focus on both drawing credible inferences and practical takeaways from his research.

Published and ongoing research focuses on three elements of financial contracting:

Financial Contracting and Coordination

Corporate Governance and Regulation

Other Related Work

Financial Contracting

Financial Contracting

Quality Transparency and Healthcare Competition

with Valeri Nikolaev, Nicholas Scott-Hearn, and Christopher Stewart, 2024.

Stanford GSB Working Paper

Transparency about the quality of goods and services offered by firms improves consumer decisions; however, it also informs competitors' strategies. We study the effect of increased transparency about healthcare service quality on the competitive dynamics among healthcare providers, focusing on the US dialysis sector. Following the 2012 mandate for public disclosure of dialysis quality data, we observe an increase in the sensitivity of consumer demand to quality. It is manifested by the immediate reduction in patient referrals to lower-quality incumbents. We use a difference-in-differences design and also exploit variation in quality induced by staggered changes in measurement methodology to show that improved quality transparency attracts new competitors into markets with historically low quality, particularly in an environment with lower barriers to entry. The enhanced transparency leads to improvements in incumbents' quality of care, as evidenced by decreased hospitalizations and increased investments in skilled labor. We find no evidence of facility managers "gaming" their quality scores. Our findings underscore the efficacy of disclosure policies in fostering competition and improving healthcare quality and quantify these effects in the context of the dialysis sector.

Firm Boundaries and Voluntary Disclosure

with Thomas Bourveau, Guoman She, and Lynn Wang, 2023.

The Accounting Review, Vol. 99, 111-141.

We study how vertical integration shapes firms' public disclosures. Theory suggests that firms can use public disclosure to coordinate with supply chain partners and predicts a substitution between vertical integration and public disclosure of future strategic plans, since the internalization of production reduces the need to publicly coordinate. Using data on the extent of vertical integration, we find that firms that become more vertically integrated reduce their public disclosures about their product strategies and that the reduction is most pronounced for vertically integrated firms with greater internalization of production and those with the largest informational and strategic frictions along the supply chain.

Stealth Acquisitions and Product Market Competition

with Vic Naiker and Christopher Stewart, 2023.

Journal of Finance, Vol. 78, 2837-2900.

We examine whether and how firms structure their merger and acquisition (M&A) deals to avoid scrutiny from antitrust regulators. There are approximately 40% more M&As than expected bunching just below thresholds that trigger antitrust review. These “stealth acquisitions” tend to involve acquisitions of private targets with terms in financial and governance contracts that afford greater scope for negotiating and assigning lower deal values such as contingent payments, additional compensation for target managers (e.g., post-acquisition employment) and extending target director and officer insurance. Consistent with stealth acquisitions reducing product market competition, we show that the equity values, gross margins, and common product prices of acquiring firms and their competitors increase following such acquisitions, but no such evidence following similar acquisitions that do undergo antitrust review. Our results suggest that acquirers successfully manipulate M&A deals to avoid antitrust scrutiny, thereby benefiting their own shareholders but potentially harming consumers due to anticompetitive behavior.

Private Communication among Competitors and Public Disclosure

2021.

Recipient of the American Accounting Association Financial Reporting Section 2020 Best Dissertation Award.

Journal of Accounting & Economics, Vol. 71, 101387.

I study how private communication among competitors affects their public disclosures. Theory suggests that competing firms can use public disclosure to coordinate, and predicts less public disclosure when there is more private communication. Using data on strategic alliances, I predict and find that firms that enter strategic alliances with competitors reduce their public disclosure, and that the reduction is more pronounced for alliances that allow for more private communication.

The Role of Executive Cash Bonuses in Providing Individual and Team Incentives

with Wayne Guay and David Tsui, 2019.

Journal of Financial Economics, Vol. 133, 441-471.

Given CEOs’ substantial equity portfolios, much recent literature on CEO incentives regards cash-based bonus plans as largely irrelevant, begging the question of why nearly all CEO compensation plans include such bonuses. We develop a new measure of bonus plan incentives, and document that performance sensitivities are much greater than prior estimates. We also test hypotheses regarding the role of bonuses in providing executives with individualized and team incentives. We find little evidence supporting the individualized incentives hypotheses, but consistent evidence that bonus plans appear to be used to encourage mutual monitoring and to facilitate coordination across the top management team as a whole.

Strategic Reactions in Corporate Tax Planning

with Christopher Armstrong and Stephen Glaeser, 2019.

Journal of Accounting & Economics, Vol. 68, 101232.

We find that firms’ tax planning exhibits strategic reactions: firms respond to changes in their industry-competitors’ tax planning by changing their own tax planning in the same direction. We document evidence of these strategic reactions in two distinct research settings that entail an exogenous increase and decrease in competitors’ tax planning. We also find evidence that strategic reactions stem from concerns about appearing more tax aggressive than industry competitors, some evidence that they stem from firms learning from the tax planning of their industry competitors, and no consistent evidence that they stem from leader-follower dynamics.

Corporate Governance and Regulation

Corporate Governance and Regulation

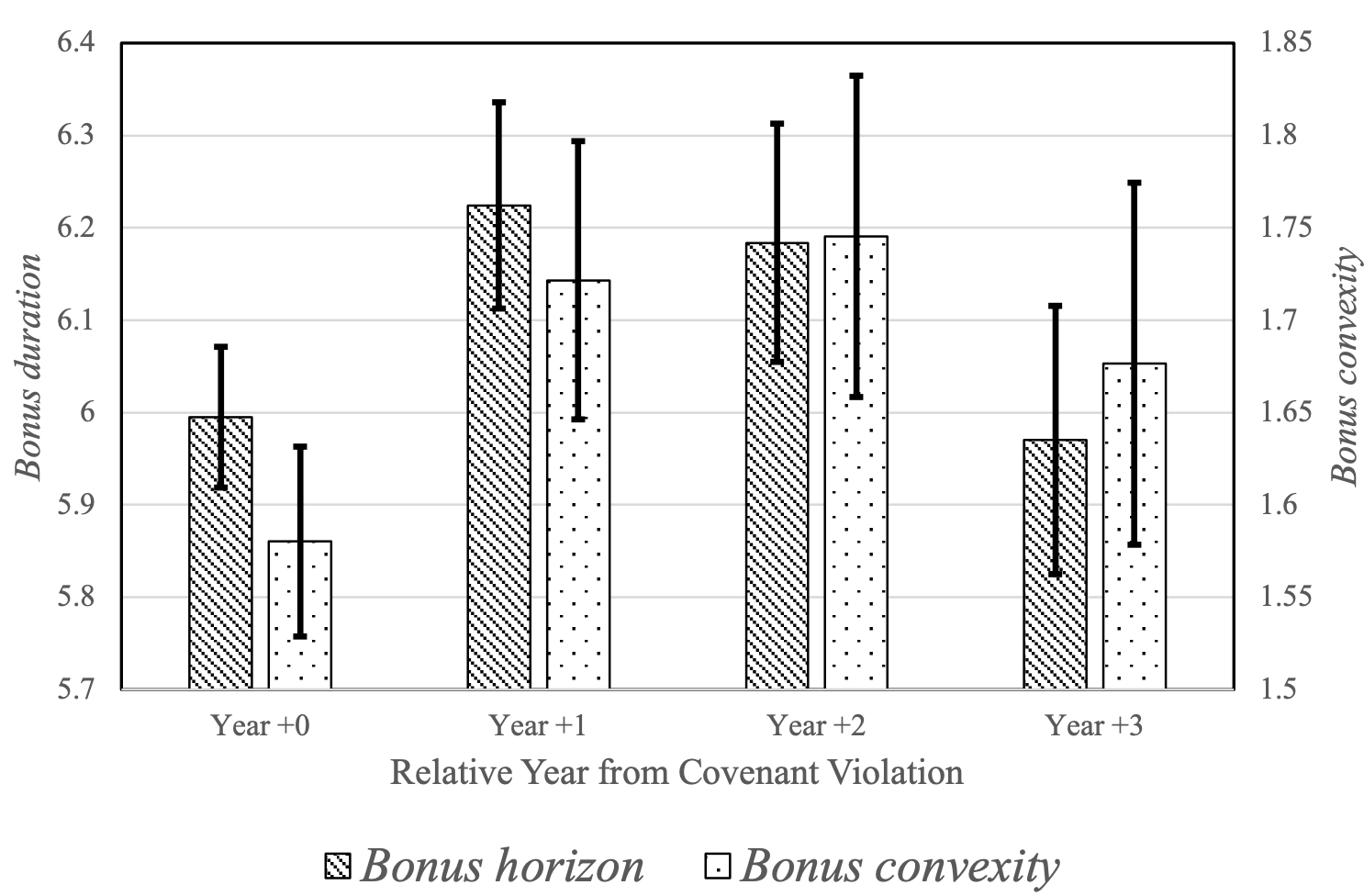

Creditor Control Rights and Executive Bonus Plans

with Christopher Armstrong, Chongho Kim, and David Tsui, 2024.

Review of Accounting Studies, Forthcoming

We study the extent to which creditors shape the executive bonus plans of their financially distressed borrowers. Financial distress can exacerbate agency conflicts between creditors and borrowers as concerns with underinvestment become more acute due to managerial myopia and debt overhang. Consequently, we expect creditors to exert their influence to ensure that these managers’ incentive-compensation plans encourage longer-term investments and directly reward outcomes that benefit creditors without exposing managers to unnecessary risk. We argue that bonus plans are an especially important way to provide these incentives because their flexibility allows creditors to more precisely (vis-à-vis equity) target specific investment objectives. We find that borrowers’ bonus plans tend to have longer horizons and more convex payouts following covenant violations, especially for those in poor financial health and where bonus plans are most likely to be effective at addressing financial distress-related agency conflicts. Our evidence suggests that creditors protect their interests by exercising their control rights to shape the incentive-compensation plans of their borrowers.

Rank-and-File Accounting Employee Compensation and Financial Reporting Quality

with Christopher Armstrong, David Larcker, and Shawn Shi, 2024.

Journal of Accounting & Economics, Vol. 78, 101672.

We use a proprietary database with detailed, employee-specific compensation contract information for rank-and-file corporate accountants who are directly involved in the financial reporting process to assess their influence on their firms’ financial reporting quality. Theory predicts that paying above-market wages can both attract employees with more human capital and subsequently encourage better performance. Consistent with audit committees structuring accountants’ compensation so as to mitigate financial misreporting that might otherwise occur, we find that firms with relatively well-paid accountants tend to issue higher-quality financial reports. Moreover, this relationship is more pronounced when firms’ senior executives have stronger contractual incentives to misreport and when the audit committee is more independent from management.

Audit Process, Private Information, and Insider Trading

with Salman Arif, Joseph Schroeder, and Daniel Taylor, 2022.

Review of Accounting Studies, Vol. 27, 1125-1156.

While the shareholder benefits of audits are well documented, evidence on whether audits can facilitate opportunistic behavior by corporate insiders is scarce. In this paper, we examine whether the audit process facilitates one particular form of opportunism: informed trading by corporate insiders. We focus our analysis on insider trading around the audit report date. We find an increase in trading around the audit report date and that the increase is abnormally large for firms that subsequently report modified opinions. The abnormal increase in trading is concentrated among officers and non-audit committee independent directors, and most pronounced in first-time modified opinions and modified opinions in years where financial results are subsequently restated. These trades are highly opportunistic: they predict restatements, and as a consequence, we show they avoid significant losses. Collectively, our findings provide novel evidence that insiders appear to exploit private information about the audit process––a process ostensibly designed to protect shareholders––for opportunistic gain.

Cost Shielding in Executive Bonus Plans

with Matthew Bloomfield, Brandon Gipper, and David Tsui, 2021.

Journal of Accounting & Economics, Vol. 72, 101428.

Executive bonus plans often incorporate performance measures that exclude particular costs—a practice we refer to as “cost shielding.” We predict that boards use cost shielding to mitigate underinvestment and insulate new managers from the costs of prior executives’ decisions. We find evidence that boards use cost shielding to deter underinvestment in intangibles and encourage managers to take advantage of growth opportunities. We also find that cost shielding tends to be elevated for newly-hired executives, and decreases over tenure. Collectively, our results suggest that boards deliberately choose performance metrics that alleviate agency conflicts.

Undisclosed SEC Investigations

with Terrence Blackburne, Phillip Quinn, and Daniel Taylor, 2021.

Management Science, Vol. 67, 3403-3418.

One of the hallmarks of the SEC’s investigative process is that it is shrouded in secrecy––only the SEC staff, high-level managers of the company being investigated, and outside counsel are typically aware of active investigations. We obtain novel data on all investigations closed by the SEC between 2000 and 2017––data that was heretofore non-public––and find that such investigations predict economically material declines in future firm performance. Despite evidence that the vast majority of these investigations are economically material, firms are not required to disclose them, and only 19% of investigations are initially disclosed. We examine whether corporate insiders exploit the undisclosed nature of these investigations for personal gain. Despite the undisclosed and economically material nature of these investigations, we find that insiders are not abstaining from trading. In particular, we find a pronounced spike in insider selling among undisclosed investigations with the most severe negative outcomes; and that abnormal selling activity appears highly opportunistic and earns significant abnormal returns. Our results suggest that SEC investigations are often undisclosed, economically material non-public events and that insiders are trading in conjunction with these events.

Accounting Quality and the Transmission of Monetary Policy

with Christopher Armstrong and Stephen Glaeser, 2019.

Journal of Accounting & Economics, Vol. 68, 101265.

We examine how firms’ accounting quality affects their reaction to monetary policy. The balance sheet channel of monetary policy predicts that the quality of firms’ accounting reports plays a role in transmitting monetary policy by affecting information asymmetries between firms and capital providers. Consistent with this prediction, we find that accounting quality moderates firms’ equity market response and future investment sensitivity to unexpected changes in monetary policy. Moreover, the former relation is amplified for firms with more growth opportunities and more financial constraints, further consistent with accounting quality moderating the transmission of monetary policy.

The Role of Executive Cash Bonuses in Providing Individual and Team Incentives

with Wayne Guay and David Tsui, 2019.

Journal of Financial Economics, Vol. 133, 441-471.

Given CEOs’ substantial equity portfolios, much recent literature on CEO incentives regards cash-based bonus plans as largely irrelevant, begging the question of why nearly all CEO compensation plans include such bonuses. We develop a new measure of bonus plan incentives, and document that performance sensitivities are much greater than prior estimates. We also test hypotheses regarding the role of bonuses in providing executives with individualized and team incentives. We find little evidence supporting the individualized incentives hypotheses, but consistent evidence that bonus plans appear to be used to encourage mutual monitoring and to facilitate coordination across the top management team as a whole.

Other Related Work

Other Related Work

Causality Redux: The Evolution of Empirical methods in Accounting Research and the Growth of Quasi-Experiments

with Christopher Armstrong, Delphine Samuels, and Daniel Taylor, 2022.

Journal of Accounting & Economics, Vol. 74, 101521.

This paper reviews the empirical methods used in the accounting literature to draw causal inferences. Similar to other social science disciplines, recent years have seen a burgeoning growth in the use of methods that seek to provide as-if random variation in observational settings—i.e., “quasi-experiments.” We provide a synthesis of the major assumptions of these methods, discuss several practical considerations for such methods, and provide a framework for thinking about whether and when quasi-experimental and non-experimental methods are well-suited for drawing causal inferences. We caution against the idea that one should restrict attention to only those causal questions for which there are quasi-experiments. We encourage researchers seeking to answer causal questions to triangulate inferences across multiple methods, research designs, and settings.

Governance of Corporate Insider Equity Trades.

with David Larcker, Brian Tayan, and Daniel Taylor, 2020.

Rock Center for Corporate Governance Closer Look Series.

Corporate executives receive a considerable portion of their compensation in the form of equity and, from time to time, sell a portion of their holdings in the open market. Executives nearly always have access to nonpublic information about the company, and routinely have an information advantage over public shareholders. Federal securities laws prohibit executives from trading on material nonpublic information about their company, and companies develop an Insider Trading Policy (ITP) to ensure executives comply with applicable rules. In this Closer Look we examine the potential shortcomings of existing governance practices as illustrated by four examples that suggest significant room for improvement.

We ask:

• Should an ITP go beyond legal requirements to minimize the risk of negative public perception from trades that might otherwise appear suspicious?

• Why don’t all companies make the terms of their ITP public?

• Why don’t more companies require the strictest standards, such as pre-approval by the general counsel and mandatory use of 10b5-1 plans?

• Does the board review trades by insiders on a regular basis? What conversation, if any, takes place between executives and the board around large, single-event sales?

Human Capital Disclosure: What Do Companies Say About their ‘Most Important Asset’?

with Amit Batish, Andrew Gordon, David Larcker, Brian Tayan, and and Courtney Yu, 2021.

Rock Center for Corporate Governance Closer Look Series.

In 2020, the Securities and Exchange Commission revised human capital disclosure rules to improve shareholder understanding of how HCM contributes to corporate value and strategy. In this Closer Look, we examine early disclosure choices that companies have made under these rules to evaluate the information they share about employment practices. We find that while some companies are transparent in explaining the philosophy, design, and focus of their HCM, most disclosure is boilerplate and lacks quantitative metrics. As such, the new rules appear to contribute to the length but not the informativeness of 10-K disclosure.

We ask:

• Are companies being evasive, or are they in the early stages of determining what information is relevant to the market?

• Will market pressure lead to better disclosure over time?

• Can a company provide informative disclosure without providing concrete metrics?

• Is there a way to describe comprehensive HCM efforts in concise and informative language, supplemented with data, in a manner that does not reveal proprietary practices?

ESG Investing: What Shareholders to Fund Managers Represent?

with Stephen Haber, David Larcker, Amit Seru, and Brian Tayan, 2022.

Rock Center for Corporate Governance Closer Look Series.

In this Closer Look, we examine individual investor perception of ESG to gauge their concern for environmental and social issues, their view of whether fund managers should use their voting power to influence ESG practices, and their willingness to sacrifice return in the advancement of ESG objectives. We find that investors are not homogenous in their viewpoints and demonstrate significant divergence based on age and wealth, with the most vulnerable investors—those who are older and those with low levels of savings—largely opposed to ESG and unwilling to risk their assets to advance these objectives, in contrast to younger, wealthy investors who are much more supportive and willing to forfeit returns. Significant differences in perception of ESG also exist within and across fund companies. The results suggest that fund managers should consider the various viewpoints of their investor base and potentially split their votes on controversial ESG-related proxy proposals to reflect the divergent interests of beneficial owners.

We ask:

• How do fund managers determine how to vote shares regarding ESG-related proxy proposals?

• How rigorous is the analysis they perform regarding the economic impact of these proposals?

• How do fund managers balance the interests of their investor base when these interests diverge?

• Would split voting improve mutual fund governance by protecting the interest of minority voters—whether that minority is in favor of or opposed to ESG?

Theory, Research Design Assumptions, and Causal Inferences

with Christopher Armstrong, 2018.

Journal of Accounting & Economics, Vol. 66, 366-373.

Ferri, Zheng, and Zou test Fischer and Verrecchia’s (2000) prediction that a reduction in investors’ uncertainty about managers’ financial reporting objectives leads to an increase in the valuation-relevance of earnings reports. They use mandatory CD&A disclosures as an arguably exogenous “shock” that provided investors with more precise information about managers’ contractual incentives and find that these enhanced disclosures increased the relation between firms’ unexpected earnings and stock returns. Using Ferri et al. as a backdrop, we discuss the implicit assumptions invoked in natural experimental research designs and the fundamental role of theory in drawing causal inferences from empirical evidence.